My Two Cents - "The Quiet Grab"

09/18/2009

While all the hubbub here in the US has centered around abominations such as cash 4 clunkers, tax credits for buying homes, and the other machinations directed at returning the US to the blissful year of 2005, other portions of the world have taken notice and have been conducting some activities of their own. They have been locking down ever-growing stockpiles of critical basic materials needed to run their economies. These strategic moves have certainly not been done in secret, but given how we spend our intellectual energies here in America, they might as well have been. Leading the pack has been China, but there have certainly been others.

Venezuelas $16 Billion Oil Deal

On 9/17/09, Venezuela President Hugo Chavez announced in a brief statement that his country had entered into a $16 billion oil deal with the Chinese to further develop the Orinoco project and ramp up Venezuelan production by 900,000 barrels per day. This agreement is separate from a similar deal inked in October of last year that promised an unspecified amount of Venezuelan production to the Chinese. The important thing to note is that Venezuelan state-owned PDVSA not only committed to ship oil East, but will essentially operate a joint venture with Beijing for the purposes of developing further reserves. At the time, Chavez was optimistic that his country would become Chinas top oil supplier.

Of important note in the oil space is the fact that the #3 supplier of oil to the US is Mexico and its production has experienced a steady decline since 2004 and is now in a full state of export destruction. While much ado has been made of the Bakken formation in the western US, some reality must be brought to bear on all the misinformation being disbursed. The US Geological Survey has stated that the formation could contain 4 billion barrels of oil. While getting every drop is impossible, lets assume for a moment that we can. Even in the throes of the worst economic contraction since the 1930s the US still burns up about 19 million barrels of oil each day. Using that as a basis, the Bakken contains a whopping 210.53 days of US supply about 7 months worth. Not really a big deal is it? For comparison, the USGS estimates Alaskan oil reserves including the North Slope to contain 90 billion barrels. Again, lets assume we can recover every drop of it. The situation here is a bit better and well get about 13 years of supply at current burn rates. Note that doesnt account for any economic growth, which carries a proportional increase in petroleum consumption under our current transportation, power, and living systems.

Keep in mind I am being purposely US centric here to frame the issue in simple terms. The recent strategic agreements the Chinese have entered into should take on a whole new significance when looking at the information through the lens of what is actually available to us domestically. Sure, they might have a large find in Brazil. Is it really safe to assume that well command it? The Dollar is already looked upon with contempt thanks to decades of abuse and there is no indication that is about to change any time soon. Unfortunately, the strategic accumulations dont stop at oil.

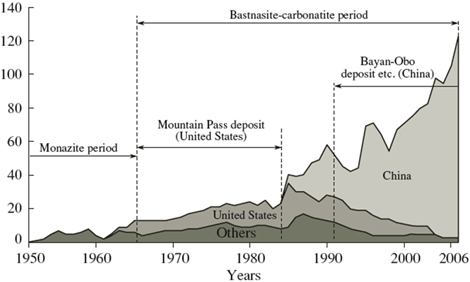

Chinas Rare Earth Metal Monopoly

While much of the talk in the US recently has shifted to green technology, there is a glaring oversight being made. These new technologies, while solving one complex problem, create another. Much of todays array of battery technology, fuel cells, wind turbines and solar panels requires an available supply of rare earth metals (REMs) for production. For the past decade and a half, the Chinese have been quietly accumulating large, unrivaled stockpiles as well as a near monopoly in the production of these critical metals. So successful were they that 95% of the lanthanide (periodic table) series metals are produced in China. These metals are used in everything from iPods to hybrid cars. Chinas 1987 pledge to become the Saudi Arabia of REMs has come true says Jack Lifton, a REM specialist. The Japanese government sees REMs being the turf for future trade wars, especially since the island country imports almost 100% of its supply from China.

As the above chart illustrates, China has a near complete stranglehold on the supply of REMs as a group and a healthy stockpile to boot. Even more importantly, mainland demand is now eating away at exports. And unfortunately, unlike oil, large deposits of REMs are not scattered all over the globe. The only real bit of good news that can be attained from the chart is that supply is still growing. Unfortunately there are no meaningful stockpiles to speak of outside mainland China.

We used to have some domestic sources of these critical metals, but unfortunately, many of those mining operations were scuttled during the price wars of the early 1990s and expensive overhauls would be necessary to get them back in production. Many industry analysts fear that Beijing will be able to affect a serious supply crunch before any meaningful competitive supply can be brought to market. Another shining example of how supply doesnt automatically appear to quench demand even though the textbooks suggest otherwise. This has resulted in a frantic scramble throughout Southeast Asia as Japanese car and electronic manufacturers try to lock down alternative sources.

Meanwhile the Chinese have sought to solidify their position as the REM capitol of the world. A state-owned investment company recently purchased a 25% stake in Arafura the Australian REM miner. In August, China Minmetals Rare Earth Company made an investment of $310 Million to lock in its dominant position in an already tight industry.

The REM situation has massive implications for the United States and our desire to go green. Without these metals, many green alternatives are not possible given current technology constraints. It also has implications for our consumption of electronic consumer goods, many of which end up in landfills when they no longer work.

Some possible conclusions that can be drawn from these activities dont paint a good picture for the continuation of activities here in the US as were used to. If the countries that supply us with many of our products are locking in stockpiles, it would be rather foolish for us to assume that theyve done so in order to continue exchanging these dwindling resources for green paper tickets as they have been doing. This becomes even more evident when one considers that much of this stockpiling didnt exist just a few years ago.

Certainly another contributing factor is that the perceptions of the dollar have grown so pessimistic that many countries are diversifying into hard assets. However, rather than creating a speculative bubble, the strategy being invoked is a longer-term accumulation strategy. They buy the dips and take delivery. This is a testament of the growing disdain of paper assets, particularly currencies. The paradigm shift, which happened not too long in the recent past, is now moving into a higher gear.

Even if this activity ends up being nothing more than a global diversification strategy, which isnt likely, then the law of unintended consequences kicks in and America will likely face nasty resource shortages as a result sooner than most are willing to admit.

Disclosure: Long Arafura

Until Next Time,

Graham Mehl is a pseudonym. He is not an âinsiderâ. He is required to use a pseudonym by the policies of his firm when releasing written work for public consumption. Although not an insider, he is astonishingly bright, having received an MBA with highest honors from the Wharton Business School at the University of Pennsylvania. He has also worked as an analyst for hedge funds and one G7 level central bank.

Andy Sutton is a research and freelance Economist. He received international honors for his work in economics at the graduate level and currently teaches high school business. Among his current research work is identifying the line in the sand where economies crumble due to extraneous debt through the use of economic modelling. His focus is also educating young people about the science of Economics using an evidence-based approach.